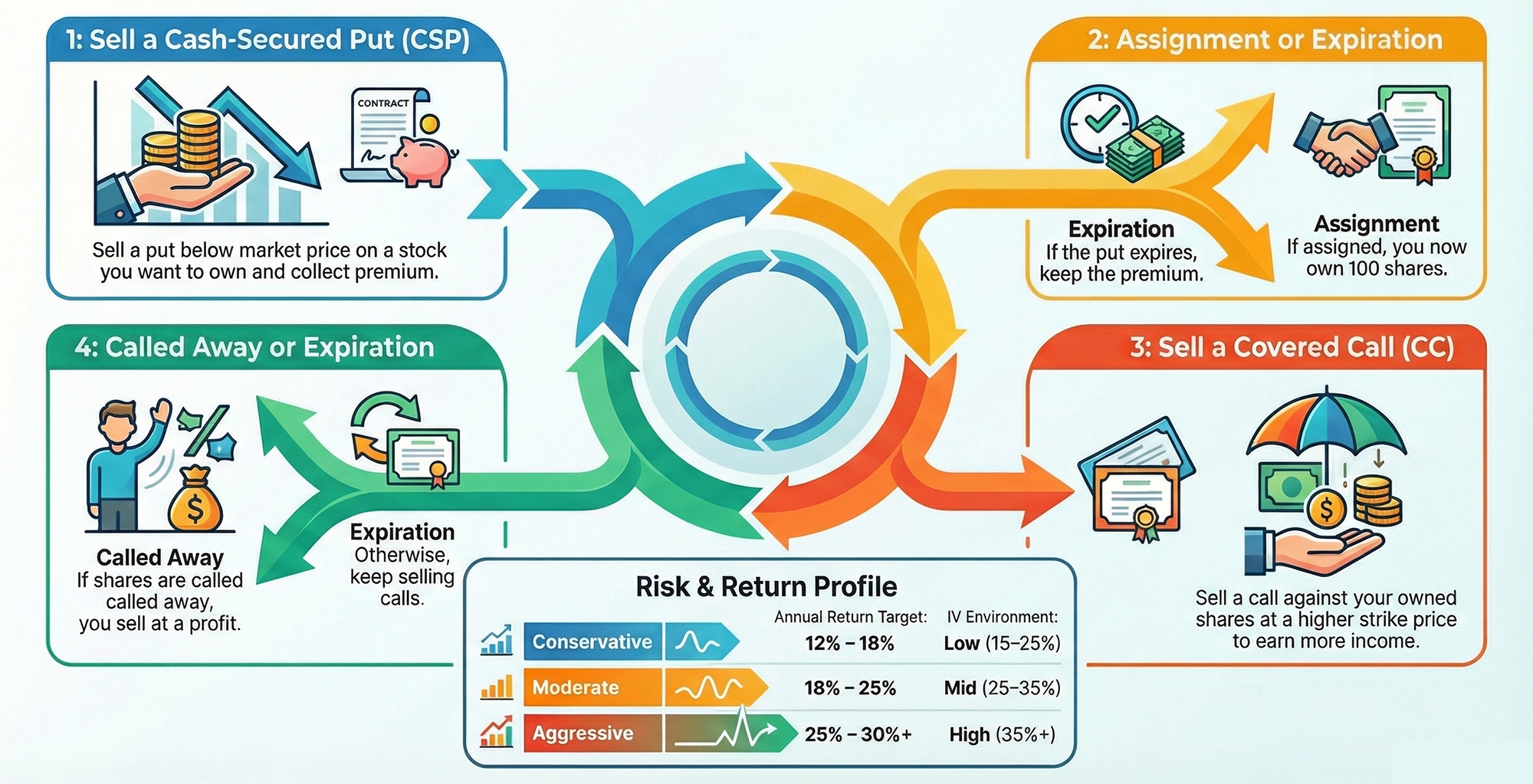

The Wheel Strategy runs in four phases:

- Sell a cash-secured put

- Manage the trade (i.e., close for early profit or roll), or get assigned shares

- Sell a covered call against those shares

- Get called away or repeat

This guide walks through each phase using a real position from entry to potential exit, so you can see exactly how the numbers work at each decision point.

Not theory.

Not vague diagrams.

Real data, real decisions, real math, so you know what to do when you’re sitting at your brokerage screen.

If you’re brand new here, I suggest starting with my What is The Wheel Strategy? guide. This article assumes you understand the basic concept and are ready to see it executed.

Table Of Contents

The Four Phases of the Wheel Strategy

Before diving into the trade mechanics, let’s cover the four phases of The Wheel Strategy:

- Phase 1: Sell a Cash-Secured Put (CSP): You sell a put, collect premium upfront, and wait. The stock either stays above your strike (ideal) or falls below it (which falls into Phase 2).

- Phase 2: Assignment or Expiration: A decision point. The CSP expires worthless (back to Phase 1), you roll for net credit (stay in Phase 1), or you get assigned (move to Phase 3).

- Phase 3: Sell a Covered Call (CC): You now own 100 shares (option contracts always represent rights to 100 shares) of the stock. You sell a call above your cost basis, collect more premium, and wait again.

- Phase 4: Called Away or Expiration: Another decision point. The CC expires worthless (sell another call, stay in Phase 3), or shares get called away (take the profit, back to Phase 1).

Phases 2 and 4 are decision points, not actions.

That distinction matters. They’re where you choose what to do next based on what the market handed you. The actions themselves happen in Phases 1 and 3.

Now let’s walk through each one with real numbers.

Phase 1: Sell a Cash-Secured Put (CSP)

The above chart displays the daily action of SSRM, a gold mining stock.

The stock is trading above both its 50MA and 200MA, indicating an uptrend.

What the CSP Phase Actually Does

Selling a CSP means that you are selling someone the right (but not the obligation) to put shares to you at the chosen strike price.

In exchange, you collect premium for taking on the risk. We consider this “risk” because we don’t know what is going to happen to the stock price:

- It could either stay above the strike price, expiring worthless

- Or, it could fall below the strike at expiration, requiring you to purchase the shares at the strike price, even if the stock price is well below the strike at expiration

The capital required to buy 100 shares at the strike is then secured and locked (reserved in your account and unavailable for other trades until the position closes).

The formula for calculating the amount of capital you’ll have locked in your account after selling a CSP follows:

Capital reserved = Strike × 100 × Number of Contracts

That premium is yours to keep regardless of what happens next.

Whether the stock goes up, goes down, or does absolutely nothing, the premium belongs to you.

Note: If you sell a CSP on SSRM with a strike price of $27 and the stock later drops to $20, then at option expiration you will be required to purchase the stock at $27, even though the current market value is significantly lower than that. This is why it is so important to learn how to properly select stocks for The Wheel Strategy!

Entering the Position

Let’s continue our example by examining options data for SSRM.

The data below comes directly from the options screener I use to scan for Wheel candidates:

- Spot price: $29.38 (current price of

SSRM) - Strike selected: $27 (8.13% below spot, a comfortable buffer)

- Delta: 0.278 (the market implies roughly a 28% probability of closing at or below this strike at expiration)

- DTE: 28 days (number of days until the option contract expires)

- Bid: $0.83

- Ask: $1.58

- Mark: $1.21

- IV: 75.95% (implied volatility)

- Annual Yield: 58.18%

- ROC: 4.46%

- Days to earnings: 75 (well clear of expiration — no earnings risk in this cycle)

Now, let’s suppose:

- We have $50,000 in our trading account

- We want to sell 2 put contracts at the $27 strike

- And, we get filled at the mark

Running the numbers:

- Capital secured: $27 × 100 × 2 = $5,400 locked

- Premium collected: $1.21 × 100 × 2 = $242

- Capital remaining: $50,000 - $5,400 = $44,600 available

- Adjusted cost basis: $27.00 - $1.21 = $25.79 per share

This trade deploys 10.8% of the account, a healthy position size (to reduce concentration risk, you typically don’t want more than 10-15% of your capital deployed into a single position).

That adjusted cost basis of $25.79 is important so let’s take a second and dissect it.

$25.79 is the effective price you’d own the shares at if assigned (i.e., stock closes below strike at expiration). We calculate the adjusted cost basis as the strike minus the premium you already pocketed.

Since we were paid (i.e., collected premium) to take on the risk of selling the option, that collected premium lowers the cost of owning the stock.

Hold onto that $25.79 number, by the way. It’s the anchor for everything that follows in Phases 3 and 4.

What about the $5,400? Does that sit idle?

Effectively, yes. That’s the price of “cash-secured.” It’s also what keeps you from getting a margin call when things go sideways.

Note: When you sell a CSP, you’re the one receiving payment. You want to receive as much as possible because you are the one taking on the risk. The ask price is the highest a buyer is willing to pay for the option at that moment. The bid is the lowest. The mark sits between them. For liquid options with tight spreads, aim to fill at or near the ask — not the bid. For illiquid options with wider spreads, start at the ask and slowly work toward the mark. Never just accept the bid for The Wheel Strategy. That’s leaving money on the table.

Managing the Trade While It’s Open

Once the CSP is open, four forces act on it simultaneously.

Let’s continue to play this example out with our SSRM position.

- The stock price moves up: Let’s suppose

SSRMrallies from $29.38 toward $31. As the $27 put moves further out of the money, its value decreases. Good for us — the position is moving toward expiring worthless, which is the ideal outcome when running The Wheel Strategy. - The stock price moves down: Now let’s suppose

SSRMdrops from $29.38 toward $27.50. As the put moves closer to the money, its value increases. Working against us. If this continues, it leads to Phase 2 (roll or assignment). - Time decay (Theta): Each day that passes, the option loses time value. As the seller, theta decay works in your favor. Even if

SSRMdoesn’t move, the option erodes a little more each day just by existing. This is the core mechanical advantage of premium selling. - IV changes: If implied volatility spikes (market panic, sector news), option premium can increase even if the stock price barely moves. This dynamic deserves its own dedicated guide, which I’ll cover in the future.

The theta time decay component is critical to understand here.

Options, by the very definition of their name, give their holder optionality. By owning a put, the holder has the right, but not the obligation, to sell the stock to you at the strike price.

Such an agreement has a contractual end date (i.e., the days to expiration, or DTE).

The longer an option is valid for, the more valuable the option, since it gives the holder optionality for a longer period of time (this is why LEAPS tend to be much more expensive to buy/sell since they are valid for a longer period of time, as compared to 30-50 DTEs).

The best possible scenario for us as CSP sellers is that either:

- The stock makes a quick run up (thereby decreasing the value of the option), and we close our position early, taking a quick profit

- The stock effectively trades sideways and each day the option slowly erodes in value until it expires worthless

In short, theta decay is our friend when applying The Wheel Strategy.

A Note on Naked Puts

Naked Puts are different from Cash-Secured Puts.

Naked Puts use leverage instead of reserved cash, which means higher potential returns and no capital sitting idle.

That sounds enticing…until you get assigned a stock and your brokerage account is raided.

I’ll cover naked puts in a separate guide, but, in general, I’d recommend against them for anyone learning the Wheel.

Three conditions must all be true before you even consider naked puts:

- You are very experienced with options and have a clear understanding of leverage

- You are already confident and proficient in running cash-secured puts

- You fully understand margin calls and forced liquidation (not just conceptually, but experientially)

If you’re reading this step-by-step guide, you are very likely not in a position to run naked puts yet.

Use CSPs. Full stop.

Phase 2: Assignment or Expiration

Phase 2 is a decision point.

You’re not taking an action here, you’re responding to what the market did since opening your position.

Three scenarios are possible. Let’s break down each of them.

Scenario A: CSP Expires Worthless

This is the ideal outcome.

Staying with our example above, SSRM stays above $27 through the 28-day cycle. The put expires worthless.

- The full $242 in premium is deposited in your account

- The $5,400 in reserved capital is freed up

- You’re back to cash, back to Phase 1

No action required at expiration if you let it run.

Alternatively, if the position reaches 50% of max profit before expiration (say the premium drops from $1.21 to around $0.60), many Wheel practitioners close early and redeploy. Same net result, faster cycle.

Note: There are pros and cons of this “turbo 50% rule”. I’ll cover them in a future tutorial.

Scenario B: Roll the Position

“Rolling” means buying back the current CSP and simultaneously selling a new one further out in time, at the same (or lower) strike.

The cardinal rule of rolling a position is that rolling must generate a net credit.

If you can’t collect more premium on the new position than you spend closing the old one, rolling is just deferring a loss and extending your time in a bad trade.

Let’s consider a hypothetical example:

SSRMhas dropped to $26.25 with 14 DTE remaining- The $27 put is now trading at $1.45

- We roll to the same $27 strike at 30-45 DTE (i.e., extend the same contract for another 30-45 days) for $1.75

- Net credit: $1.75 - $1.45 = $0.30

Acceptable. We’ve bought more time and collected additional premium without spending anything out of pocket.

If no net credit is available (meaning you’d have to pay more to close the old position than you’d collect opening the new one), that is a debit roll. Don’t do it. You’d be paying the market to extend a losing trade. Accept assignment instead.

Note: There is a downside to rolling, even if it generates a net credit. You’re continuing to lock up your capital and lowering your effective annual yield. The funds could be better deployed elsewhere. Sometimes it’s wise to just accept your position didn’t work out, close it, take the loss, and move on.

Scenario C: Accept Assignment

Okay, now let’s say:

SSRMhas dropped to $26.25.- The contract expires today

- There is no way way to roll the contract for a net credit

What happens now?

You get assigned the stock.

You are required to buy 200 shares (2 contracts × 100) at $27 per share:

- Cash leaving account: $27 × 200 = $5,400 (already reserved in your account, no additional capital required)

- Adjusted cost basis: $25.79 per share (strike minus premium collected)

- What you own: 200 shares of

SSRMat an effective entry of $25.79

Here’s the thing:

Assignment is not a failure.

I know because my stomach dropped the first time I got that assignment notification — even though I understood intellectually what was happening. I was refreshing my brokerage app watching that strike approach, and when the assignment hit, my first instinct was that I’d done something wrong.

I hadn’t. The math made that clear immediately.

SSRM is trading at $26.25…but your effective entry is $25.79. You’re already above water, before you’ve sold a single covered call!

The premium you collected from selling the original CSP bought you that buffer. That’s not an accident; that’s the strategy working exactly as designed.

You didn’t get stuck, your capital simply rotated from cash to shares of SSRM.

Now we move to Phase 3.

Phase 3: Sell a Covered Call (CC)

We now own 200 shares of SSRM with an adjusted cost basis of $25.79 per share.

Remember back in Phase 1 when we sold a CSP on SSRM without actually owning the stock?

Conceptually, we can do the same thing now that we own the stock, only we call this process a covered call.

The Mechanics of Selling a Covered Call

You own the shares — now you sell someone the right to buy them from you at a specific price.

The strike you choose should be at or above your adjusted cost basis.

This is non-negotiable. If SSRM gets called away below $25.79, you exit at a loss.

The whole point of selling CCs in this phase is to generate additional premium while locking in a profitable exit if the shares are called away.

Selling a covered call:

- Generates additional premium

- Further reduces your adjusted cost basis

- Obligates you to sell your shares at the strike price if the stock closes above it at expiration

The SSRM Covered Call Example

Suppose SSRM stabilizes around $27.00 after assignment.

Instead of selling a CSP, we’ll sell 2 covered calls at the $28 strike, 30 DTE.

Let’s suppose we collect $0.60 per share in premium for selling the CC.

Running the numbers:

- Premium collected: $0.60 × 200 shares = $120

- New adjusted cost basis: $25.79 - $0.60 = $25.19 per share

- Capital deployed: 200 shares at $27 market value = $5,400 in shares (which we already own)

No additional cash is required for the covered call phase. The shares themselves are the collateral.

Now we sit back and wait for either:

- The contract to expire worthless

- The stock to close above the strike at expiration and the shares called away

One Consideration: When to Stop Selling Covered Calls

Let’s suppose SSRM goes on a strong run, perhaps breaking above $35 on high volume.

If that happens you may want to pause CC selling and let the stock compound upward.

Selling covered calls on a running stock caps your upside.

Sometimes the right answer is to simply hold.

This is a judgment call, not a mechanical rule. It’s also one of the more nuanced decisions in the Wheel — experience is the only way to develop a feel for it.

Phase 4: Called Away or Expiration

Phase 4 mirrors Phase 2. You’re responding to what the market did while you waited.

Two outcomes are possible when the covered call reaches expiration.

Scenario A: CC Expires Worthless

If SSRM stays below $28 through expiration:

- The call expires worthless

- You keep the $120 in CC premium

- Adjusted cost basis drops to $25.19

- Sell another covered call (i.e., back to Phase 3), or if the stock is trending up, let it run and appreciate in value

The cycle of premium collection continues until the shares are called away, or you choose to close the position outright (i.e., sell the shares manually via a market order, limit order, stop market order, etc.)

Scenario B: Shares Called Away

If SSRM rallies past $28 at expiration, then your shares will be called away at the $28 strike (even if the stock is trading higher than $28 at the expiration date).

This is the “clean exit” we are looking for when running The Wheel Strategy:

- Exit price: $28.00 per share

- Adjusted cost basis: $25.19 (after two rounds of premium, one from a CSP and another from CC)

- Profit per share: $28.00 - $25.19 = $2.81

- Total profit: $2.81 × 200 shares = $562

Profit Analysis

Here’s the full summary of our example running The Wheel Strategy on SSRM:

| Stage | Amount |

|---|---|

| CSP premium collected | $242 ($1.21 × 200 shares) |

| CC premium collected | $120 ($0.60 × 200 shares) |

| Total premium collected | $362 |

| Capital secured | $5,400 |

| Exit price (called away at $28) | $5,600 (200 shares × $28) |

| Total profit | $562 |

| Return on capital | ~10.4% |

| Approximate duration | 8-12 weeks |

| Annualized yield | 45-67% |

Note: We’re assuming a simple, non-compounded annualized yield here.

Honestly, this isn’t a bad outcome for a position that initially went against us by falling below the strike.

They key here is that:

- The premium from selling the CSP cushioned the entry

- The covered calls lowered the cost basis further

- We exited at a profit on a stock were were happy to own

After being called away, the $5,400 in capital is now $5,600 , plus the $362 in total premium collected across both phases. Back to cash. Back to Phase 1.

After being called away, our portfolio value is now $50,562, a total portfolio increase of 1.12%.

In a diversified portfolio, you’re running multiple cycles simultaneously:

- Some in the CSP phase

- Some working through assignment

- Some collecting CC premium

Portfolio-level income smooths out considerably compared to any single position.

That’s compounding, one premium at a time.

The Wheel in Practice: What to Expect

The Wheel Strategy is mechanically simple, but let me be honest about where the difficulty actually lives:

It’s not in the mechanics. You can learn the mechanics in an afternoon. The hard part is discipline — choosing the right stocks, sizing correctly, and not panicking when assignment happens.

Three things the SSRM example demonstrated:

- Premium collection immediately reduces your effective cost basis. You entered at $25.79, not $27.00.

- Assignment on a properly-selected stock is a rotation event, not a crisis. The capital kept working, just in a different phase.

- The cycle generates return even when the trade “goes sideways”. The put was breached, and the position still exited profitable.

Obviously, not every Wheel cycle will look as clean as this simplified example!

Some stocks will keep declining after assignment. That’s why stock selection and position sizing matter far more than the mechanics. The mechanics are the easy part.

In reality, here’s what your first few cycles of The Wheel Strategy will likely feel like:

- The mechanics click quickly

- Selling the put, entering the order, watching theta work — that part becomes comfortable fast

- What takes longer is the emotional calibration

- The first time you watch a position drift toward your strike, you’ll question whether you sized correctly

- The first assignment notification will still give you pause, even if you intellectually know it’s fine.

These anxieties and jitters will flatten over time. Yes, there is a learning curve. But it flattens and becomes easier the more cycles you run.

Your mileage will vary, and that variance lives almost entirely in how well you select the underlying stock, not in how well you execute the options trades themselves.

Get the stock selection right and the mechanics handle themselves. Get it wrong, and no amount of clean execution saves you.

For a deeper grounding in the foundational principles, start with What is The Wheel Strategy? which covers stock selection philosophy, personality fit, and the mindset required to run this consistently.

Disclaimer

WheelMetrics is an educational resource, not financial advice. WheelMetrics is not a registered investment advisor, broker-dealer, or financial planner. Everything here, including articles, newsletters, stock screening results, options setups, market commentary, is for educational and informational purposes only. Options trading carries substantial risk, and you can lose some or all of your capital. You're solely responsible for your own investment decisions. Consult with a qualified financial advisor before making any trades.